What is Blockchain Technology?

Blockchain technology has emerged as a revolutionary concept since its inception in 2008, primarily associated with the digital currency Bitcoin. The underlying principles of blockchain are rooted in the need for a secure and transparent method of recording transactions without the necessity for a central authority. At its core, blockchain functions as a decentralized ledger, allowing multiple participants to access, verify, and update records in real-time, thereby promoting trust and security across transactions.

The foundational element of blockchain technology is its structural organization. Data is stored in blocks, which are linked together to form a chain. Each block contains a set of transactions and a cryptographic hash of the previous block, ensuring that any alteration to the data is easily detectable. This immutable feature of blockchain contributes significantly to its integrity, making it a reliable choice for various applications beyond cryptocurrency, including supply chain management, healthcare, and finance.

One of the primary reasons for the growing prominence of blockchain technology in various industries is its capacity to enhance efficiency and reduce costs. By eliminating intermediaries, organizations can streamline operations, minimize errors, and expedite transactions. Furthermore, decentralized networks diminish the risks associated with central points of failure, enhancing overall security and resilience.

Understanding blockchain technology is increasingly essential in today’s digital economy. As businesses and governments alike explore the potential of this innovative system, a solid grasp of its functionalities can provide a significant competitive advantage. By embracing blockchain, organizations not only stand to improve their operational efficiency but also prepare for a future where decentralized solutions play a vital role in economic interactions.

The Core Components of Blockchain

Blockchain technology, often synonymous with cryptocurrencies, encompasses a range of essential components that work synergistically to create a secure and decentralized ledger system. These core components include blocks, chains, nodes, and miners, each playing a critical role in maintaining the integrity of the blockchain.

At the heart of this technology are blocks. A block is a digital container that stores a list of transactions. Each block consists of several key elements: a timestamp, transaction data, and a cryptographic hash of the previous block, which ensures the chronological order and connection between blocks. This inter-linking creates what is known as the blockchain itself. Once a block is filled with transaction data, it is added to the blockchain, forming an unalterable part of the ledger.

The chain is the foundational structure of blockchain technology, linking individual blocks in a secured manner. This chain is transparent and accessible to all participants in the network, enhancing trust between users. The data housed within the chain is immutable; once data is recorded, it cannot be modified without altering all subsequent blocks, making tampering virtually impossible.

Nodes are another critical component, representing the devices that store and maintain copies of the blockchain. Each node operates a version of the blockchain, allowing for a decentralized network where no single entity holds all the power. This contributes to the security and resilience of the blockchain, as nodes continuously communicate and validate transactions.

Finally, there are miners, whose role is crucial in validating new transactions before they are added to a block. Through a process known as mining, miners solve complex mathematical problems that secure the network and maintain the integrity of the blockchain. In return for their efforts, miners are rewarded with cryptocurrency, incentivizing them to uphold the system’s security.

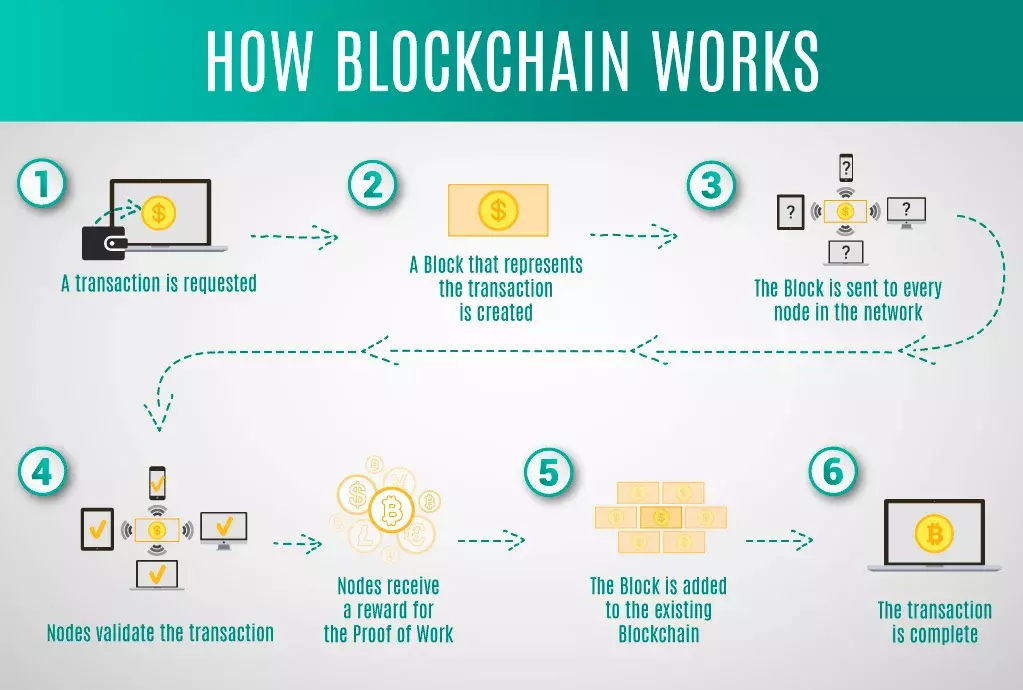

How Blockchain Technology Works

Blockchain technology operates as a decentralized and distributed ledger that enables transparent and secure recording of transactions across a network of computers. This innovative system begins with the creation of a transaction, which typically involves parties transferring assets or data. Initially, the transaction is generated, including relevant details such as the sender, recipient, and amount. At this point, cryptographic algorithms are utilized to ensure that the transaction data is secure and tamper-proof.

Once a transaction is created, it requires validation by network participants, often referred to as nodes. These nodes are responsible for verifying that the transaction adheres to the established rules of the network. This verification process may vary based on the consensus mechanism employed by the blockchain. Common mechanisms include Proof of Work (PoW) and Proof of Stake (PoS), among others. In PoW, miners solve complex mathematical problems to validate transactions, while in PoS, validators are chosen based on the number of coins they hold and are willing to “stake” as collateral.

After validation, the transaction is bundled with others and organized into a block. Each block contains a cryptographic hash of the previous block, along with a timestamp and transaction data. This chaining of blocks is fundamental to blockchain technology as it creates an immutable record of transactions. Once a block is filled and validated, it is added to the existing chain, which is then updated across all nodes in the network, ensuring that every participant has the most current version of the ledger.

This decentralized system promotes trust, as no single entity has control over the entire blockchain. It enhances security and reduces the possibility of fraud, making blockchain technology a revolutionary solution in various industries, from finance to supply chain management. By engaging in this multi-step process of transaction creation, validation, and recording, blockchain technology offers a reliable framework for conducting digital transactions in an increasingly interconnected world.

Types of Blockchain: Public, Private, and Consortium

In the realm of blockchain technology, three primary categories are widely recognized: public, private, and consortium blockchains. Each type possesses distinct characteristics that cater to varied use cases, advantages, and disadvantages, which are essential for prospective users to consider when selecting a blockchain solution.

Public blockchains, such as Bitcoin and Ethereum, operate on a decentralized network where anyone can join and participate. These blockchains are open-source, allowing users to inspect and verify the code. The key advantage of public blockchains is their high level of transparency and security, achieved through widespread consensus mechanisms. However, this openness can also lead to scalability issues, resulting in slower transaction speeds, particularly during peak usage periods.

Conversely, private blockchains restrict access to a select group of participants. These blockchains are typically managed by a single organization or consortium, which has full control over who can participate in the network. The primary advantage of private blockchains lies in their enhanced privacy and faster transaction processing times, as the consensus mechanism can be simplified. However, this centralization raises concerns regarding trust, as the controlling entity may act against the interests of the wider community.

Lastly, consortium blockchains represent a hybrid of public and private types. These blockchains are governed by multiple organizations, making them ideal for businesses seeking to collaborate while maintaining some level of control over the network. Consortium blockchains combine the advantages of decentralization with improved efficiency and privacy, but they may still face challenges related to governance and consensus among the participating entities.

Each type of blockchain has its unique features, and understanding these differences is crucial for organizations as they navigate the landscape of blockchain technology. The choice between public, private, and consortium blockchains ultimately depends on specific business objectives, desired levels of privacy, and the need for decentralization.

Applications of Blockchain Technology

Blockchain technology, originally conceived as the underlying framework for cryptocurrencies like Bitcoin, has now transcended its initial purpose to significantly impact numerous sectors. Its core attributes, including transparency, decentralization, and security, have facilitated innovative applications in various industries beyond finance. One prominent example is supply chain management. Companies are using blockchain to create transparent and tamper-proof logs of goods as they move through the supply chain. This advancement not only enhances traceability but also boosts accountability among suppliers, mitigating fraud and ensuring compliance with regulations. Major organizations, such as Walmart, have implemented blockchain solutions to track the origin of food products, allowing for quick identification during food safety issues.

Another significant application of blockchain technology is in the healthcare sector. Here, blockchain provides a secure method to store and share patient data, ensuring it is accessible only to authorized personnel while maintaining privacy. This can dramatically reduce medical errors and enhance efficiency in patient care. Recent pilot programs, such as those deployed by IBM with their Watson Health initiative, have demonstrated how blockchain can facilitate interoperability among healthcare systems, streamlining patient management and reducing costs associated with administrative burdens.

Moreover, blockchain technology is making waves in contract management through smart contracts, which are self-executing contracts with the terms directly written into code. This technology is particularly beneficial for real estate transactions, where it can simplify the buying and selling process, reducing delays and closing costs. For instance, the Estonian government has embraced blockchain for various public services, enabling secure and efficient citizen transactions.

In conclusion, the applications of blockchain technology extend far beyond cryptocurrencies, with significant implications for sectors such as finance, supply chain management, and healthcare. Its transformative potential is evident through real-world examples and case studies, demonstrating that blockchain can enhance efficiency, security, and transparency in various industries.

Benefits of Blockchain Technology

The implementation of blockchain technology presents numerous advantages that significantly address various challenges faced by businesses and consumers alike. One of the primary benefits of blockchain is increased transparency. By providing an immutable and shared ledger, all parties involved in a transaction can access the same information simultaneously. This transparency reduces disputes and promotes trust among participants, creating a more reliable environment for conducting business.

Another fundamental benefit of blockchain technology is enhanced security. Traditional data storage often relies on centralized systems, making them vulnerable to breaches and cyberattacks. In contrast, blockchain operates on a decentralized architecture, utilizing cryptographic techniques that secure the data and make it extremely difficult for unauthorized individuals to alter information. This enhanced security is vital for maintaining the integrity of sensitive information across various sectors, including finance and healthcare.

Furthermore, blockchain offers improved traceability, particularly in supply chain management. Each transaction or transfer of assets recorded on the blockchain is time-stamped and permanent, enabling stakeholders to track the movement of goods from their origin to their destination. This ability to trace sources and verify authenticity is essential for combating fraud and ensuring compliance with regulatory standards.

Additionally, the cost reduction potential of blockchain technology cannot be overlooked. By eliminating intermediaries and streamlining processes, businesses can achieve significant savings on transaction fees and operational costs. For instance, blockchain can facilitate direct peer-to-peer transactions, allowing for quicker settlements and reduced reliance on traditional banking systems.

In summary, the benefits of blockchain technology, including increased transparency, enhanced security, improved traceability, and potential cost savings, offer compelling reasons for its adoption across various industries. As organizations continue to recognize and leverage these advantages, the transformative impact of blockchain on the global economy becomes increasingly evident.

Challenges and Limitations of Blockchain Technology

Blockchain technology has revolutionized the way transactions and data are managed; however, it is not without its challenges and limitations. One of the most prominent issues is scalability. As the number of users and transactions increases, many blockchain networks struggle to maintain speed and efficiency. The original Bitcoin blockchain, for instance, has a maximum transaction capacity that can lead to slower confirmation times and higher fees during peak demand. This raises questions about the technology’s ability to accommodate widespread commercial use.

Another significant challenge is the evolving regulatory landscape. Different countries have varying degrees of acceptance for blockchain applications, leading to regulatory uncertainty. Governments are often apprehensive about the implications of decentralization and the potential for illicit activities associated with cryptocurrencies. This uncertainty complicates the development and implementation of blockchain solutions, as companies need to navigate an ever-changing regulatory environment.

Moreover, energy consumption is a pressing concern, particularly for proof-of-work blockchains. The process of mining new blocks requires considerable computational power, which translates into high energy usage, raising environmental questions. While some networks are shifting to more energy-efficient consensus mechanisms, the overall energy footprint of blockchain remains a topic of discussion among environmental advocates.

Lastly, security vulnerabilities present another limitation. While blockchain networks are generally considered secure, they are not immune to attacks or bugs. For example, smart contracts—self-executing contracts with the terms of the agreement directly written into code—can have security flaws that hackers may exploit. In addition, the irreversible nature of blockchain transactions makes it challenging to recover from any breaches or errors.

Addressing these challenges is vital for the broader adoption of blockchain technology. As stakeholders collaborate to find solutions, it will be crucial to ensure that the benefits of this transformative technology can be realized without compromising security, efficiency, or compliance with regulatory standards.

What is Blockchain Technology’s Future?

As blockchain technology continues to evolve, several trends signal significant advancements that are poised to reshape various industries. One of the primary focuses of future developments will be on scalability solutions. Current blockchain networks often face challenges regarding transaction speed and capacity. Innovations like sharding and layer-two solutions, such as state channels and sidechains, aim to enhance the scalability of these networks. By improving throughput and reducing latency, these advancements will allow blockchain systems to support a greater volume of transactions seamlessly, thereby addressing one of the critical limitations observed today.

In addition to scalability, the integration of blockchain technology with artificial intelligence (AI) is an emerging trend that holds considerable promise. AI can enhance blockchain’s capabilities by optimizing transaction processes, improving security protocols, and even automating smart contracts. The synergy of these technologies could lead to more efficient data management systems, enabling real-time decision-making based on secure and decentralized data sources. As AI continues to mature, its incorporation into blockchain-based applications will undoubtedly unlock new potentials and create new use cases across various sectors.

Furthermore, the evolving regulatory landscape presents both challenges and opportunities for blockchain technology’s future. Governments worldwide are beginning to recognize the importance of implementing regulations that foster innovation while protecting consumers. As a result, we can expect a more standardized approach to blockchain technology regulations in the coming years. Striking a balance between regulatory compliance and technological advancement will be crucial for the sustainable growth of blockchain. Establishing clear frameworks will not only enhance trust among users but also pave the way for broader adoption across industries.

In summary, the future of blockchain technology is promising, characterized by advancements in scalability, integration with AI, and a more defined regulatory framework. These developments are set to enhance the technology’s usability and effectiveness, ultimately contributing to its pervasive influence across various sectors.

Conclusion: The Impact of Blockchain Technology

I think you may have understood what is blockchain technology. In reflecting upon the intricacies of blockchain technology, it becomes evident that its significance cannot be overstated in our rapidly evolving digital landscape. The previous sections have elucidated how blockchain serves as a decentralized ledger, offering transparency, security, and efficiency that traditional systems often lack. This innovative technology has the potential to revolutionize various sectors, from finance and supply chain management to healthcare and governance.

The transformative power of blockchain lies in its ability to eliminate intermediaries, thereby reducing costs and streamlining processes. By fostering a more secure and transparent environment, blockchain enhances trust among participants in transactions. This aspect is particularly crucial in industries where accountability and traceability are paramount. Furthermore, the rise of smart contracts, which automate and enforce agreements without the need for intermediary intervention, is reshaping the dynamic of contractual relationships.

<punderstanding age,=”” alike.=”” allows=”” also=”” and=”” as=”” being=”” blockchain=”” blockchain-based=”” businesses,=”” by=”” capabilities=”” complexities=”” currencies,=”” decentralized=”” digital=”” effectively.=”” enable=”” essential=”” finance,=”” for=”” further=”” governments=”” in=”” increasingly=”” individuals,=”” innovations.

Moreover, the ongoing developments in blockchain applications, such as non-fungible tokens (NFTs) and decentralized applications (dApps), signify a shift towards a more interconnected and efficient economy. By acknowledging and embracing the benefits of blockchain, individuals and organizations can position themselves to adapt to future changes and capitalize on emerging opportunities.

In conclusion, blockchain technology stands as a pillar of the future’s digital economy, profoundly influencing how we interact, transact, and authenticate in an increasingly connected world. As the understanding of this technology deepens, it paves the way for innovative solutions that will shape our collective future.